| A key moment in The Hitchhiker's Guide to the Galaxy comes when the ultimate improbability drive suddenly calls into existence a sperm whale and a bowl of petunias, high in the stratosphere above a lonely planet. As they whiz downward toward the end of their brief and improbable existence, the whale excitedly comes up with words for things like "air" and "tail" and "wind" and, lastly, "ground." Meanwhile, according to the guide: The only thing that went through the mind of the bowl of petunias as it fell was: "Oh no. Not again!" Many people have speculated that if we knew exactly why the bowl of petunias had thought that we should know a lot more about the nature of the universe than we do now.

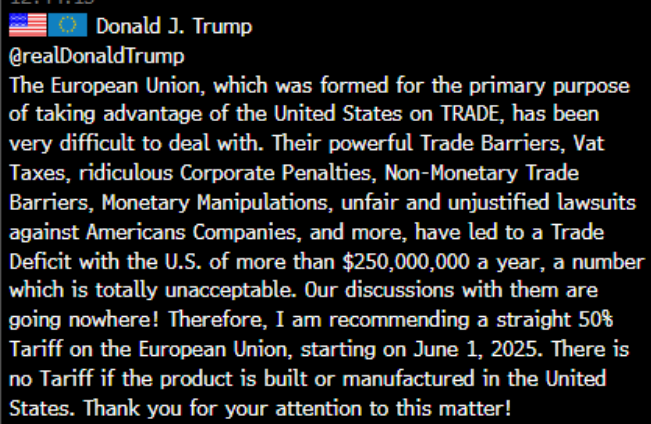

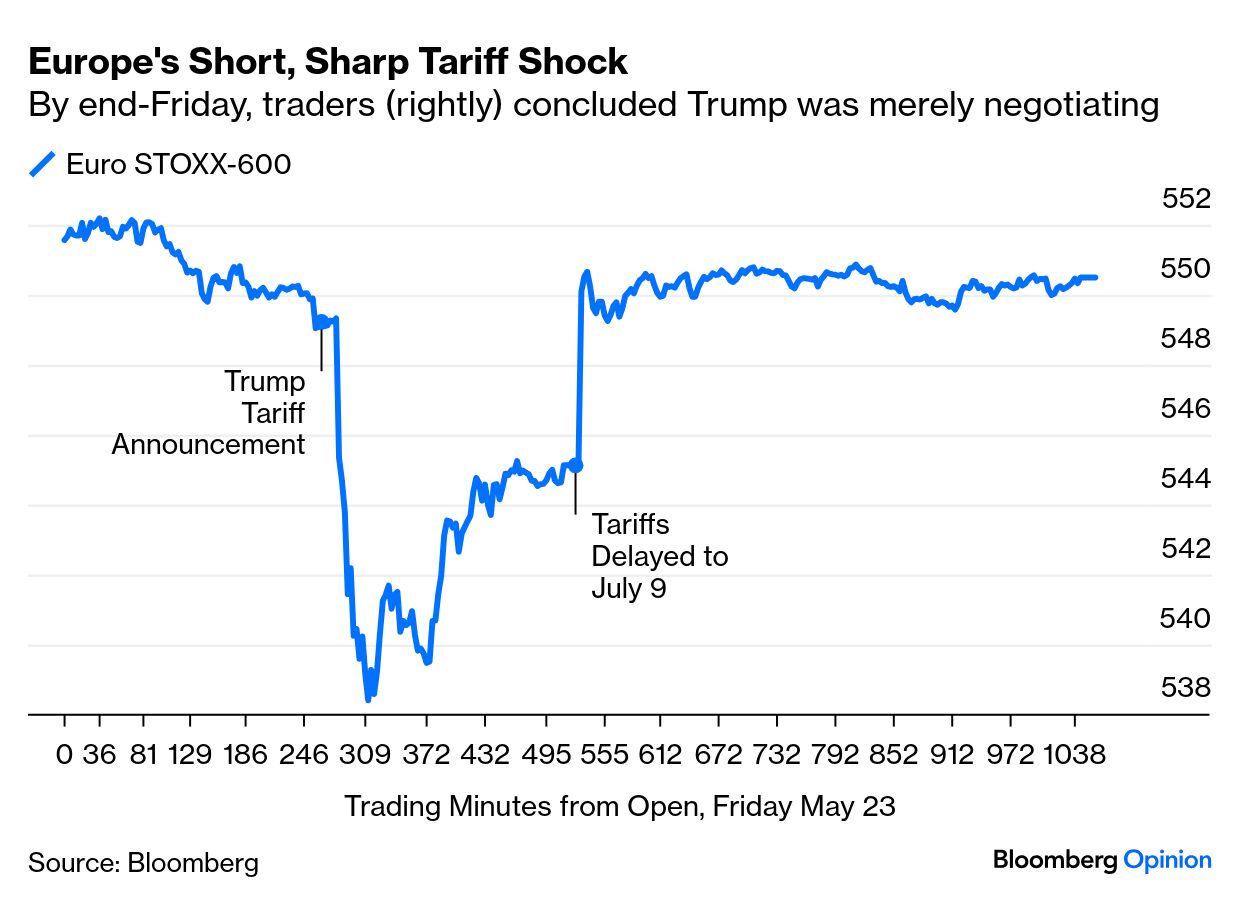

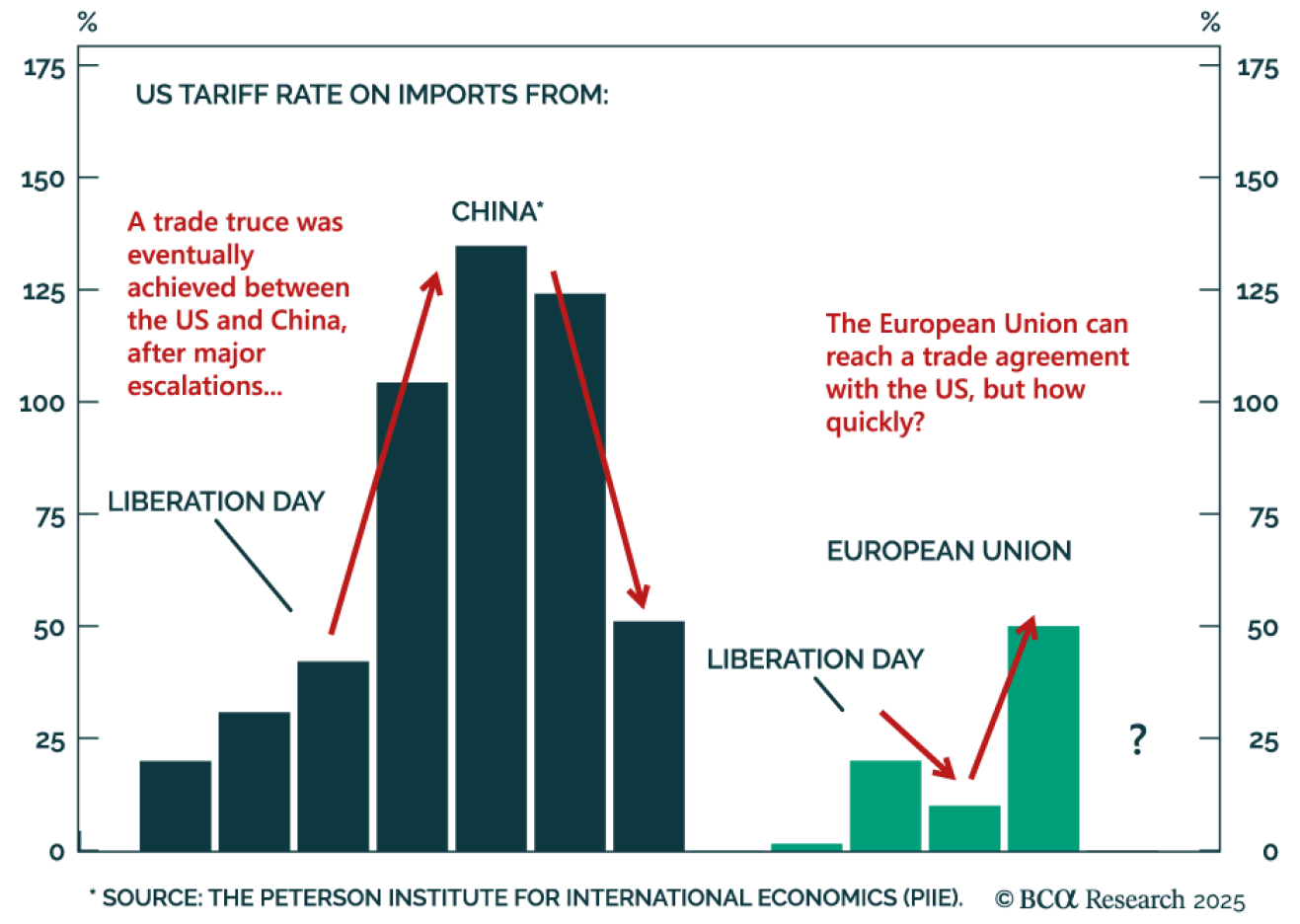

We can all sympathize with the petunias after a long weekend of US trade policy toward Europe. Tariffs of 20% were on pause until July; then raised on Friday to 50% as of June 1; then delayed again on Sunday to 50% as of July 9. This was the Friday presidential pronouncement: This would have as big an impact on the global economy as a sperm whale hitting the ground from a great height. Yet we've been through a cycle of adopting and delaying tariffs in just three days, repeating the exact same cycle that played out in April. "Oh no. Not again!" European stocks' round trip was spectacular. After selling off, the Stoxx 600 had regained most of the ground by the close on Friday, assuming that President Donald Trump would soon climb down. Sunday brought news of the delay following Trump's chat with the European Commission's Ursula von der Leyen, and Monday saw the remaining damage made good. In sum, for the stock market, nothing had happened. The selloff barely lasted longer than the petunias: This is BCA Research's schema of the progress of tariffs on China and the EU under the current administration. Any of these rates would mean the biggest restrictions on trade since the Second World War: Trump's statement was soon dismissed as a negotiating tactic. Jaded investors no longer think the US is serious about trade policy. Analysts noted that the president said he was merely "recommending" a 50% tariff, and that his announcement came immediately before his representatives were to meet with EU counterparts. Deutsche Bank AG's Maximilian Uleer reacted as follows on Friday: After multiple threats by the US administration that have ultimately not been carried out, markets are no longer (neither do we) taking them at face value. After the 20% tariff announcement on "Liberation Day," the STOXX-50 was down almost 4%. After today's 50% announcement, the STOXX-50 closed down less than 2%. It seems most likely that those tariffs are not here to stay.

He was proved right. The general attitude of exasperation and cynicism that followed Trump's announcement was largely justified. That said, it's significant that the US president has returned to the tactic of threatening imminent and self-defeating tariffs, even though previous uses of the gambit delivered few if any benefits. And the US has genuine animus toward the EU. As Tigress Capital Partners' Jean Ergas puts it, Trump is not in a trade conflict with the EU so much as seeking reparations. He has repeated the claim that the EU was established for "the primary purpose of taking advantage of [he's previously said "screwing"] the US." It's difficult to work out why he thinks this, but his belief is a fact and the EU must deal with . To this basic antipathy, Jordan Rochester of Mizuho International Plc lists more tangible grievances, none of which is directly about tariffs: 1. The sizeable non-tariff barriers (various studies estimate equivalent to anything between a 5%-13% non-tariff barrier for trade with the EU).

2. The wider EU trade surplus with the US since Trump's first term, despite the 2018 "deal" to buy more US products to reduce the surplus.

3. The EU's digital services tax – a 3% levy on digital revenues with a high impact on US tech firms.

4. The EU's regulatory zeal on US products (e.g. iPhone and USB-C).

5. The US's lower reliance on EU trade for its own manufacturing process (EU exports more high-end finished goods such as cars to the US), making it a standoff it can perhaps afford to hold out on for longer.

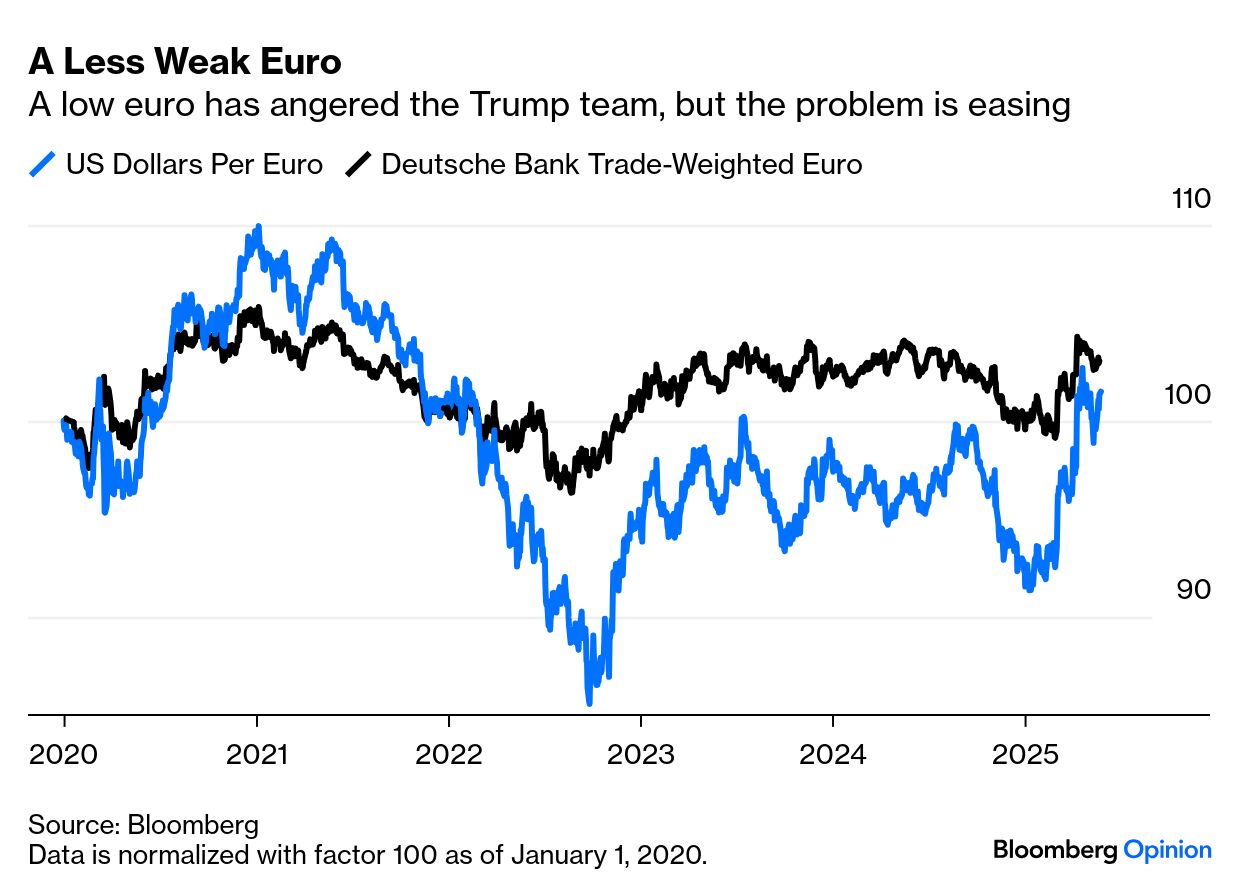

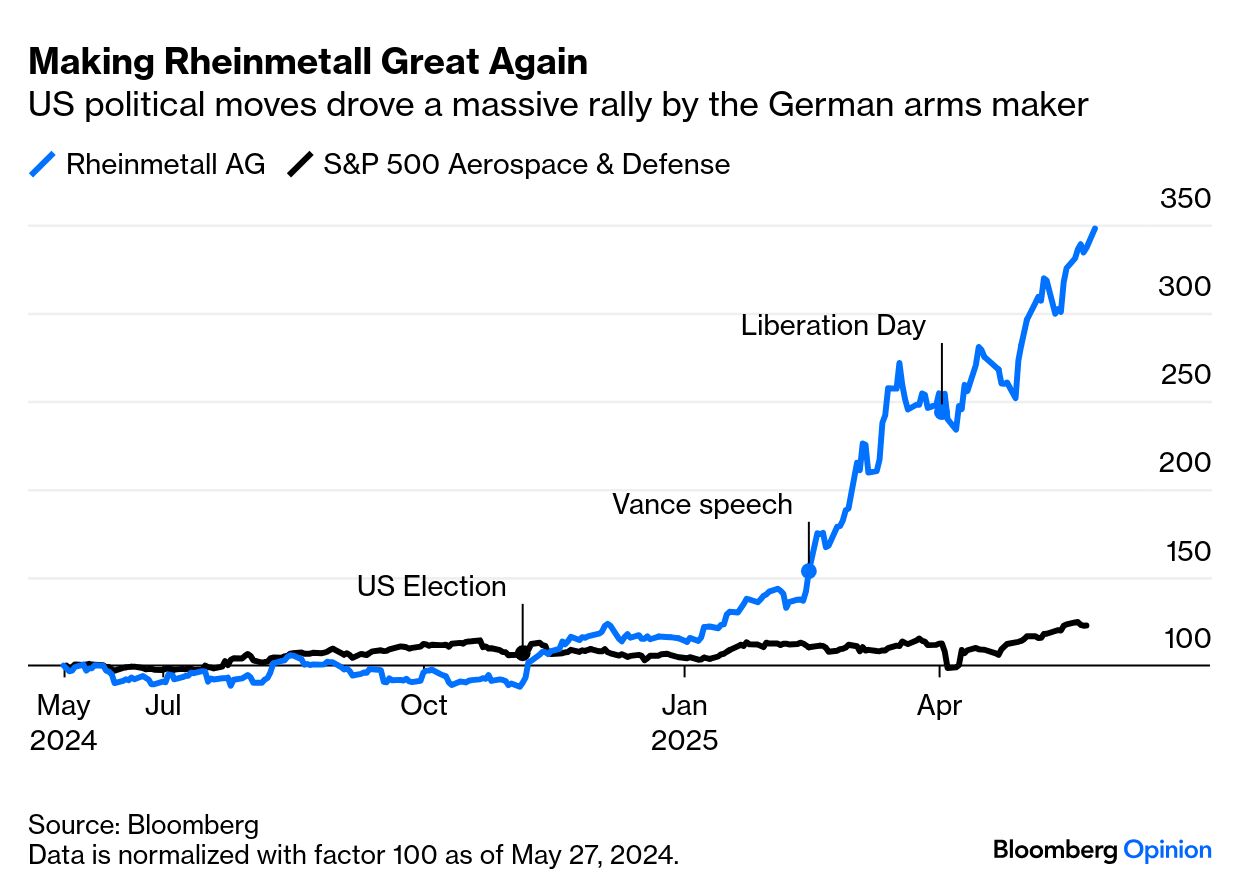

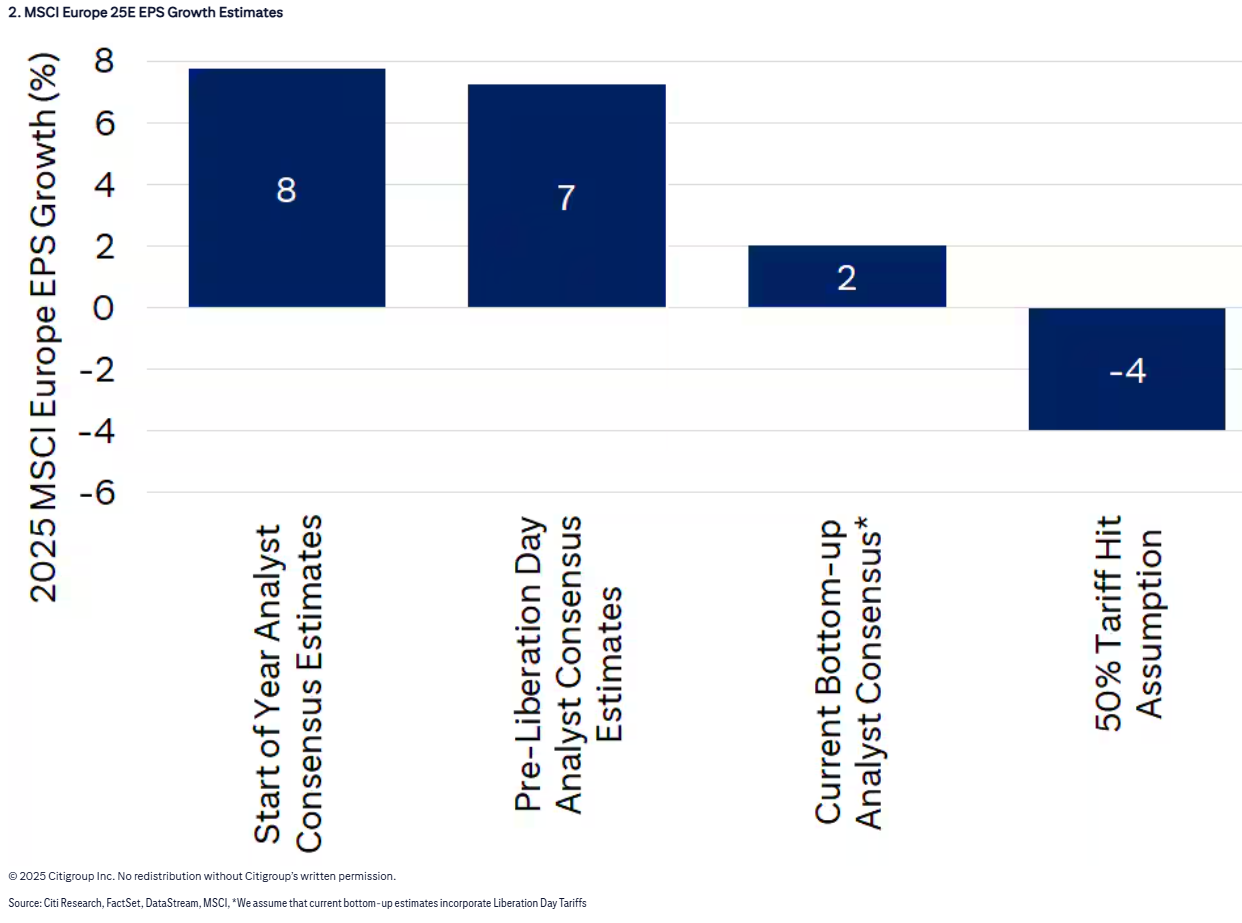

It's possible to quibble with this list. The non-tariff barrier figure includes Europe's value-added tax, levied at the same rate on EU goods. Recent euro weakness can be seen as a non-tariff barrier, but appreciation under Trump is alleviating the problem: A 50% tariff would damage Europe's economy seriously, just as Trumpian foreign policy had prompted an overdue German shift to expansive fiscal policy and an increased defense budget. This has driven a remarkable rally for Germany's biggest weapons contractor, Rheinmetall AG, only intensified by the latest announcement: Faced with a determined US opponent, the EU's most obvious concessions are not really about trade. They could buy more liquefied natural gas from the US, or promise to spend some of its defense budget with US suppliers — which might imply that the Rheinmetall rally is overdone. The current 10% tariffs have already hit European earnings expectations, as illustrated here by Citigroup Inc.'s Beata Manthey: This episode also suggests the US is not trying to isolate China, as at one point seemed plausible. To quote Barclays Plc's Ajay Rajadhyaksha: On April 9, when the president announced the first 90-day moratorium on all countries except China, market sentiment was that the US was looking to isolate China on trade. That argument took a serious hit when the reciprocal tariffs on China dropped to just 10% (in addition to the 20% fentanyl tariffs). But is the US truly prepared to go through June with 10% reciprocal tariffs on China and 50% on the EU? We don't think so.

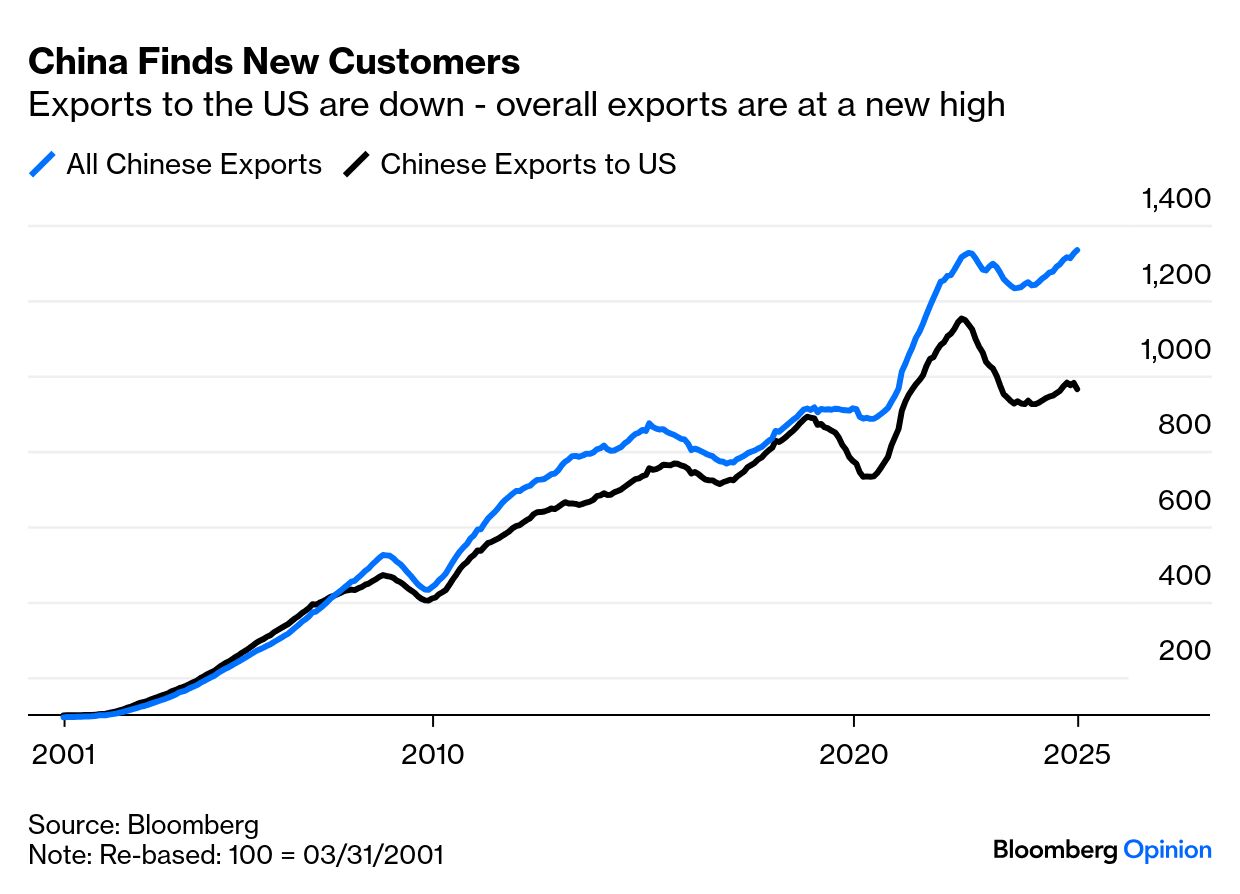

Trump pulled back, but the plan remains to levy higher tariffs on the EU than on China from July 9. That won't isolate China, where April data show that it is finding new customers. US exports are down badly, but total exports are at an all-time high: Alejandra Grindal of Ned Davis Research said that all the major economies to report for April had positive year-on-year growth and only Brazil came in below its average over the past three years. It's possible that the impact of tariffs has been exaggerated, or that the US doesn't have the leverage it thinks it has. Either way, we're entitled to complain that the cycle of tariff threats is happening again. |