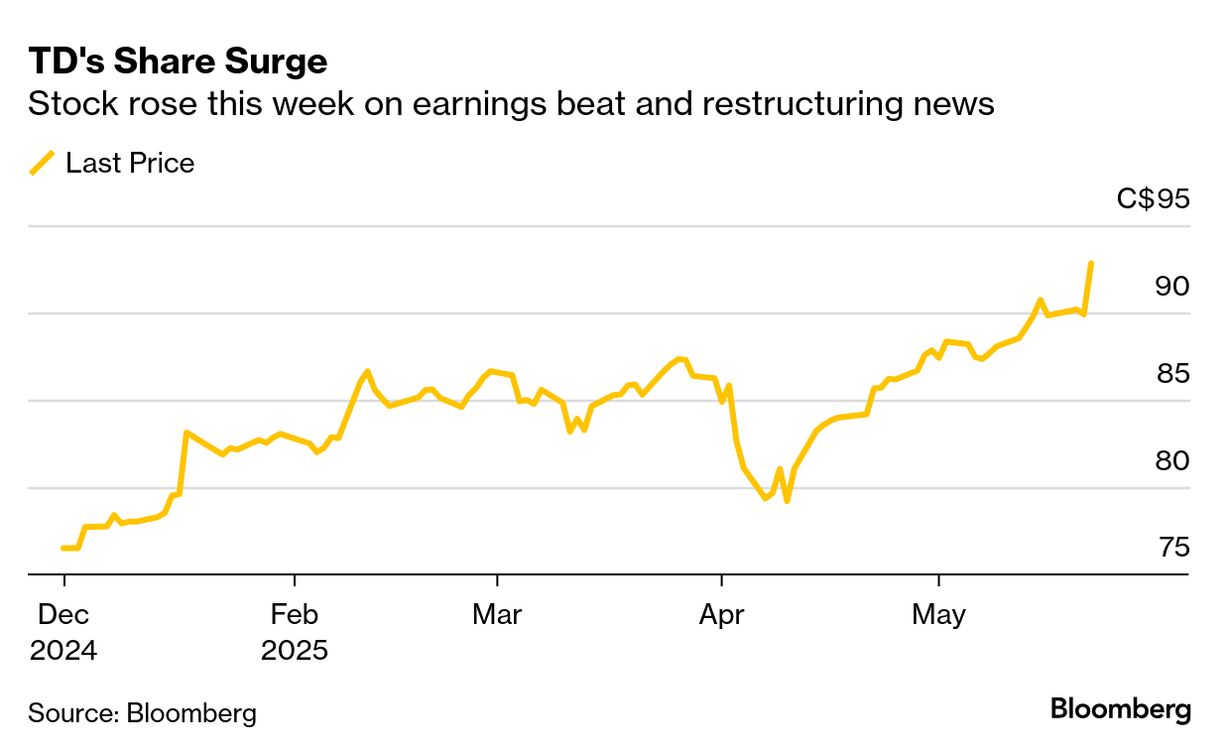

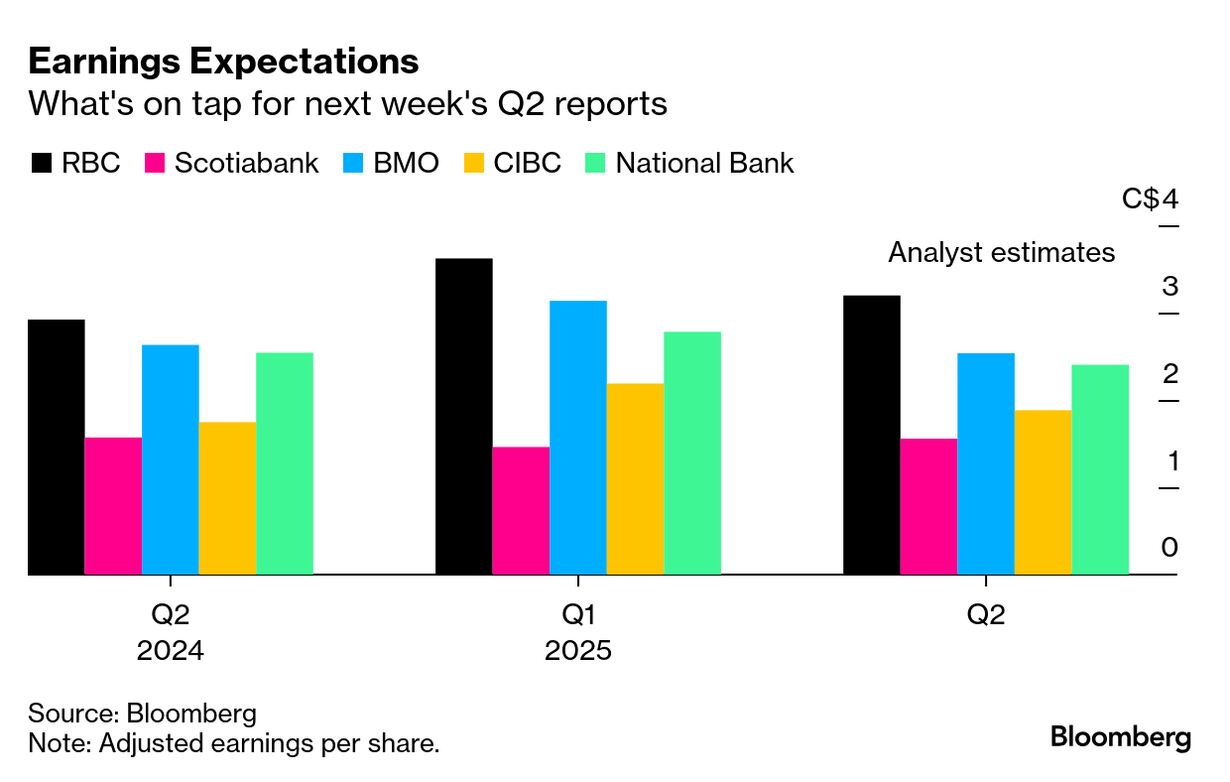

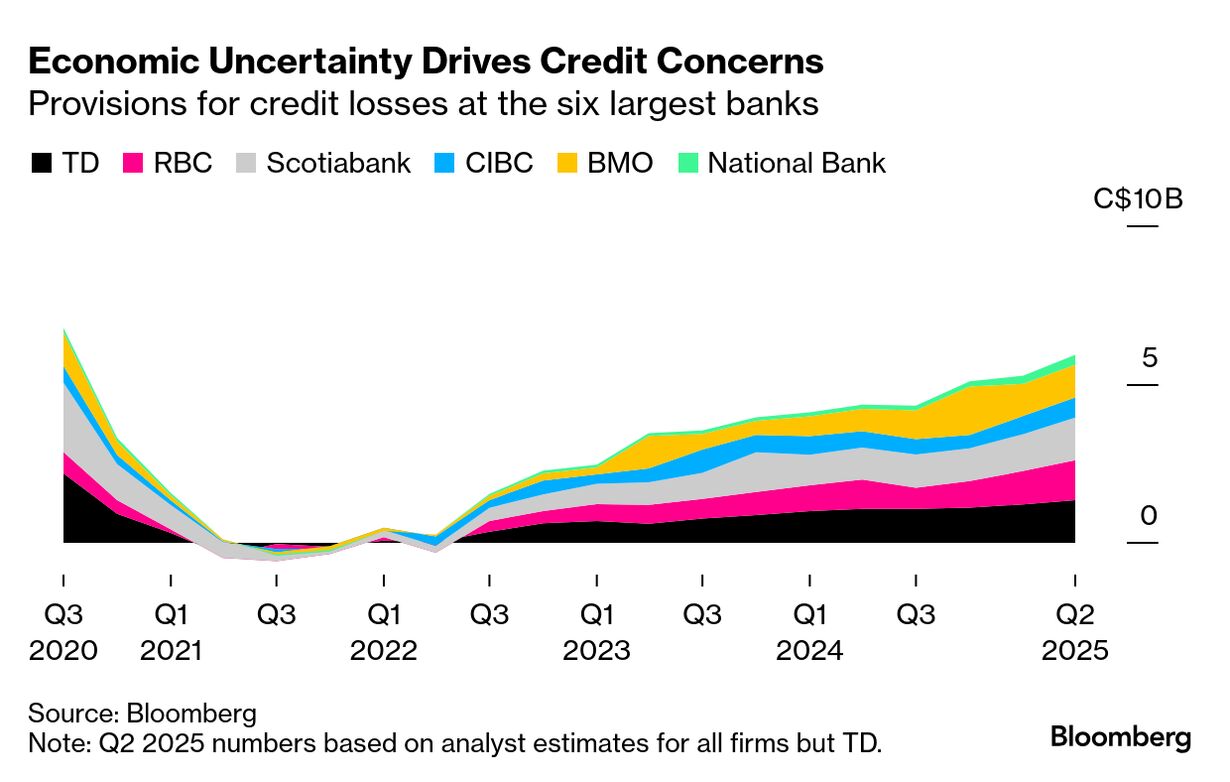

| Call it a bank earnings amuse bouche. Toronto-Dominion Bank was the first Canadian lender to release its fiscal second quarter results, offering just enough for analysts and financial journalists to chew on as we await updates from the rest of the big banks next week. TD has its own (ahem) unique set of issues at the moment. It's in a transition period after reaching a $3.1 billion settlement over US anti-money-laundering failures. New Chief Executive Officer Raymond Chun is leading an overhaul of strategy, and the board is looking for a new chair. Chun plans to update investors on the path forward in late September, but the country's No. 2 bank is already slashing expenses. TD will cut about 2% of its workforce, or roughly 2,000 jobs, as part of a restructuring program it started in the second quarter. But when it comes to how economic turmoil is shaping TD's core lending businesses — mortgages, credit cards and personal and commercial loans — it's in much the same situation as its peers. So its earnings report may provide a decent hint about what's to come from the other banks next week. TD set aside a bit less money than analysts expected for possibly bad loans in the quarter, but it's still preparing for what could be some very gloomy days ahead. The bank earmarked C$1.34 billion ($975 million) for possible credit losses in Q2, up 25% from the same period last year. For loans that are still in good standing, it provisioned C$395 million. Banks tend to increase their provisions for credit losses against performing loans when the economic outlook is poor — building up their reserves so they can absorb the impact of higher customer defaults in the future. "What is certain is uncertainty, as credit provisions continued to trend higher, weighed by the overhang of US tariffs, affecting the economic trajectory and the outlook on credit," Jefferies Financial analyst John Aiken wrote in a report. Higher loan-loss provisions "could be a common theme that will resonate across the remainder of Q2 reporting." And that, Aiken said, is despite the fact that the picture for actual bad loans is, well, not that bad — or at least getting better. TD reserved less for impaired loans than it did in the first quarter, with the figures shrinking across most of its asset classes, from real estate to credit cards to commercial loans, according to Chief Risk Officer Ajai Bambawale. "They're not large dollars, but I'd call them quite symbolic because it's really telling us that if you keep this tariff issue aside, we were really seeing peak PCL and good quality," he said, adding that lower interest rates have helped borrowers. Ah, but you can't leave the tariff issue aside (trust me, we would love to!). Week by week, Donald Trump's trade war is chipping away at confidence and investment in certain Canadian industries. The economy is far from a disaster but it's clearly softening. Economists surveyed by Bloomberg now see a shallow recession this year, with unemployment rising to 7.2% by year-end. As a result, Aiken expects other banks will also increase their provisions for credit losses on performing loans — as they do when they're expecting a storm. Aiken forecasts a 28% jump in overall provisions compared to Q1, and about a 59% hike from a year earlier. Tough to swallow. |