| Humans think in terms of narratives. We're hot-wired to do so; condense something complicated into a story, and we understand it more easily. That raises the risk of over-simplification and narrative fallacy — a notion from Nassim Taleb — in which we grab hold of a version of events and allow it to color incoming data. Much market analysis is about comprehensible stories, without fallacy. It's not easy. Any good tale, even if it's untrue, can change prices — and thereby the economy surrounding it — if enough people believe it. That creates possible turning points. When everyone is positioned for one narrative, and something happens to cast doubt on it, there is money to be made. That might be the case at present, as the facts allow starkly different explanations. The S&P 500 had a great, broad advance Tuesday. It's up 19% since its nadir on April 8, one of the biggest rallies ever for the index. But it's equally true that the S&P is lower than six months ago, and from the close on the day after the election. How should we view it? Here are the narratives driving markets now: - The Bond Vigilantes Have Gone Away

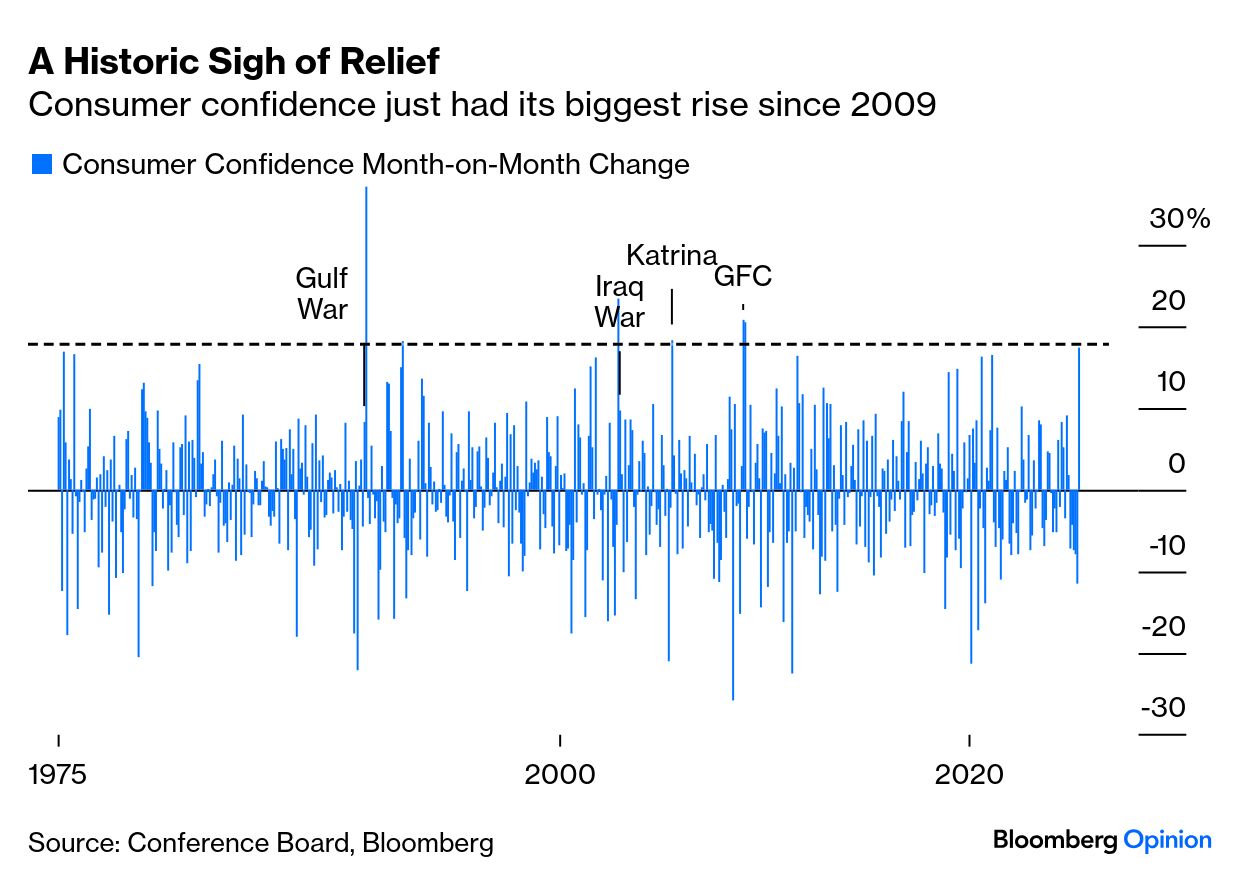

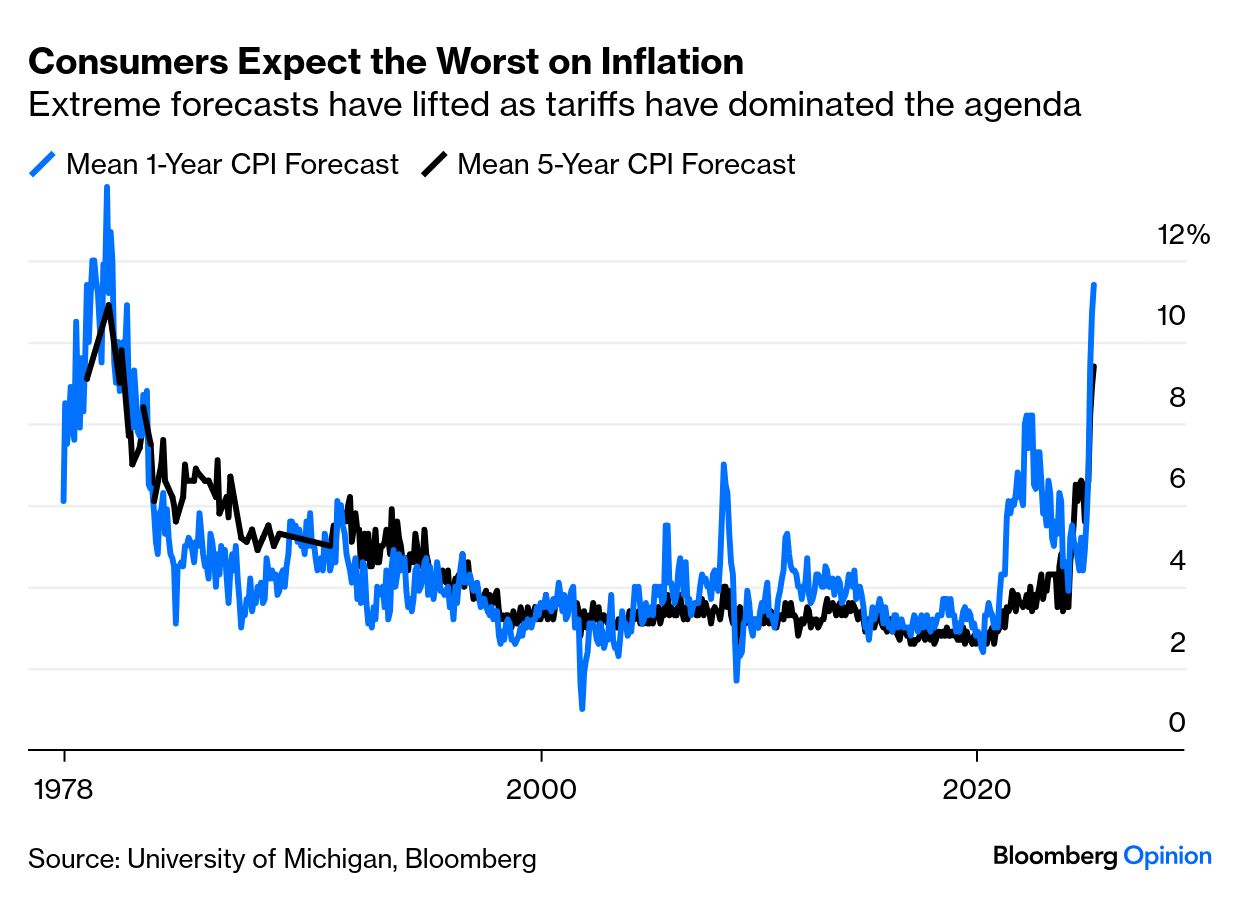

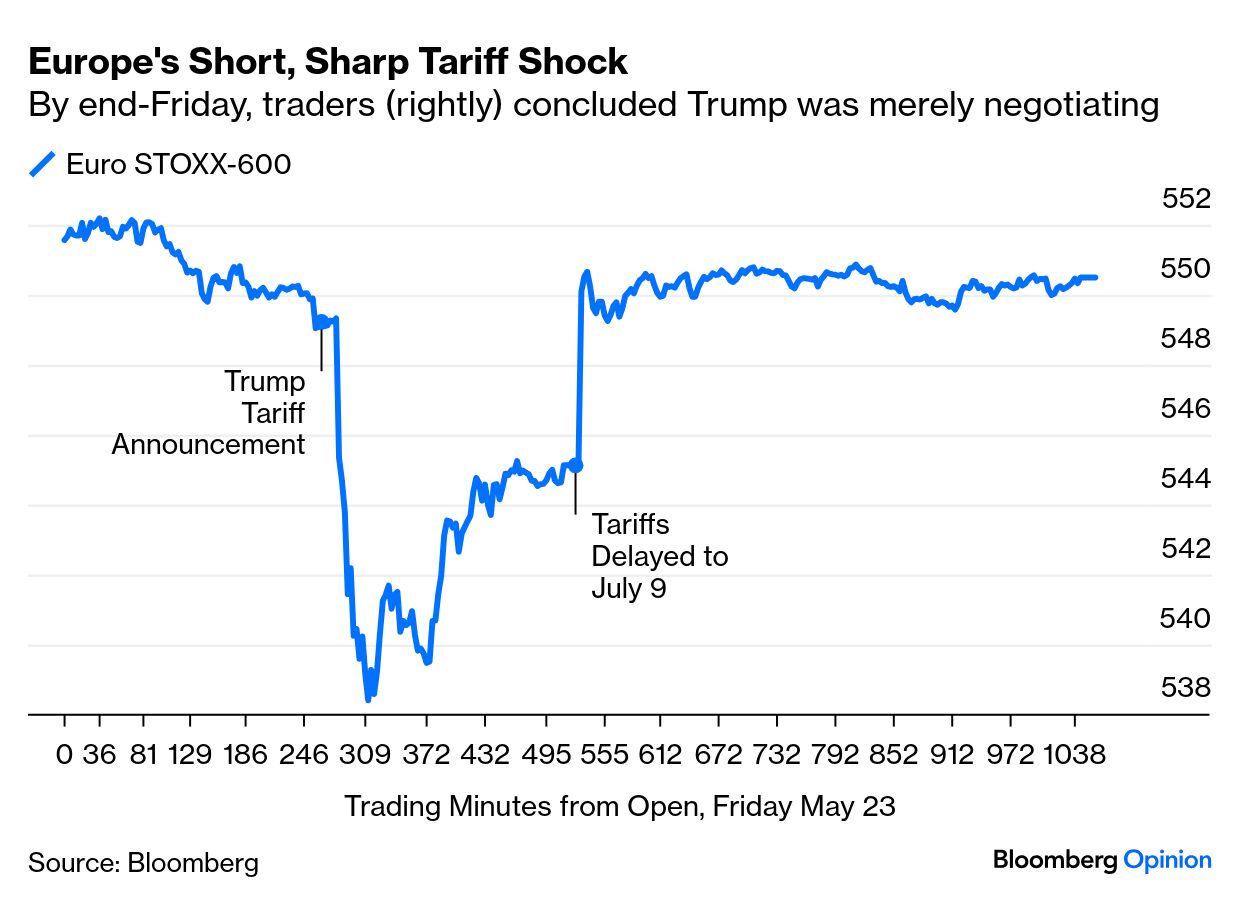

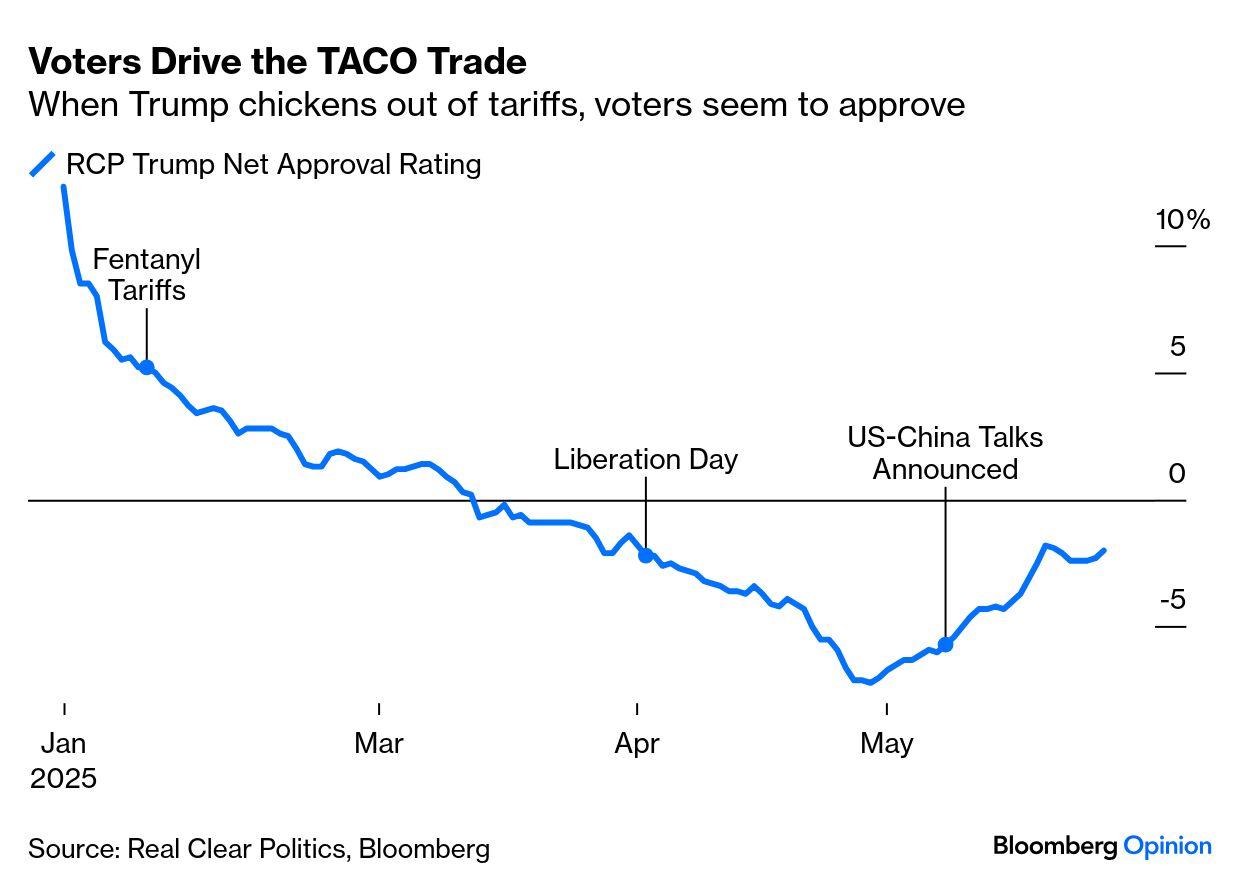

This is a reversal of last week's "The Bond Vigilantes are back, and this time they really mean it" story. Both infer the narrative from the price; long bond yields spiked across the world a few days ago because the vigilantes were balking at governments' excessive demands. Now that yields are down, there's a twist in the tale and supposedly vigilantes aren't so bothered. This is what happened to 30-year Japanese yields after the government announced it was considering fiddling with issuance to borrow less over the longest terms — a move that reduces supply for the longest bonds and thereby their yields: An immense buildup in JGB yields remains intact, but US investors were heartened. Then Tuesday's auction of Treasuries was much better received than last week's, and bond investors decided the danger was over. They were helped by a reappraisal of the narrative surrounding the One Big Beautiful Bill, which involves both large tax cuts and significant spending curbs on politically sensitive programs like Medicaid. Last week, that was seen as irresponsibly boosting the deficit. Matthew Klein of the Overshoot newsletter points out that expectations of a much higher deficit were based on the technicality that the first-term Trump tax cuts were due to end. As everyone assumed that a Republican Congress would extend those cuts, the likely impact of this package is much tougher on the deficit than expected — even more so if tariffs really generate some revenue: Some of the cuts look politically untenable, and the package must survive the Senate. But the most accurate narrative for now might be: "Bond vigilantes are stirring, but governments can still just about keep them in check." Americans continue to be the world's spenders of last resort, and opinion surveys suggest they are angry and confused. After startling declines in consumer confidence that troughed in April with tariffs dominating the news, the Conference Board showed the biggest monthly leap of confidence since 2009. Beyond that, in the last 50 years only the months after the end of the first Gulf War, the fall of Saddam Hussein's statue in Baghdad, and Hurricane Katrina have seen bigger rebounds: Rather than by a war or a hurricane, confidence this time was driven by one politician's plan, and then his change of mind. The Conference Board also had decent news on inflation expectations, which ballooned after the "Liberation Day" tariff announcements. Forecasts remain uncomfortably high, but consumers almost always predict worse inflation than actually results: These numbers are at least more palatable than the frankly horrifying predictions that consumers gave to the University of Michigan. Those numbers showed consumers bracing for a repeat of the 1970s: That's a scary narrative, and people are only happy for an excuse (such as the Conference Board data) to abandon it. They have another excuse, too... This one was christened by friend and former colleague Rob Armstrong of the Financial Times. TACO stands for Trump Always Chickens Out. I wish I'd thought of that one. Traders have noted the president's propensity to make threats, scare the market, and then pull back. Now they are skipping the selloff, and assuming that Trump always caves. The fast-disappearing 50% tariffs on the European Union was the greatest example, as we showed yesterday: Adding ballast to the TACO case is the link between consumer confidence, angst over tariffs, and presidential approval. Voters approve of Trump chickening out on tariffs, and traders assume that the president has also noticed this. Maybe his improving approval rating emboldened him to threaten a new tariff on the EU: The TACO assumption is that henceforward Trump 2.0 will be like Trump 1.0: tax cuts, deregulation, and fiscal largesse. One problem with this is that if the bond vigilantes have really been appeased, that implies no fiscal stimulus for everyone to feast on; two positive narratives are in direct conflict. There is another problem. If his threats are merely negotiating tactics and seen as such, then they're useless in a negotiation. Trump has broadcast his enthusiasm for tariffs for decades before he entered politics, and even after his climbdowns, tariffs are the highest in decades. It's not clear he will always back off. Which leads to a third problem: that TACO traders are too confident by half. Peter Atwater of Financial Insyghts suggests the trade is now so brazen as to signal trouble ahead: The open air grifting feels like it has now reached bubble status. The collective invulnerability is palpable with participants at all levels believing it is unstoppable. No one believes the crowd's moral compass will swing back. Put simply, it feels like something big is about to happen.

|